Published:

Jan 16, 2019

Updated:

June 12, 2023

Understanding the ins and outs of IPO pricing can help you know what to expect on the day of your IPO.

The day of your IPO is the culmination of years of hard work and preparation. While being a public company comes with its own set of challenges, the day of your IPO is a cause for celebration. The business that began in your garage will now be traded alongside companies like Apple and Amazon. The day of an IPO is full of excitement—but also anxiety. Understanding the ins and outs of what will happen to the price of your shares on the day of your IPO can help you know what to expect during this exhilarating time.

This article will explain how an IPO works and describe the critical moments on the day of the IPO with an emphasis on pricing. To provide the necessary context, the article will also describe some key events related to pricing that occur in the months and weeks leading up to an IPO. In addition, the article will analyze first-day returns for public offerings.

Before considering what happens in the days leading up to an IPO, it is important to understand how the IPO process works. Broadly speaking, in an initial public offering, a private company sells a portion of its ownership to the public to raise capital and increase liquidity for current shareholders. The following chart offers a more detailed look at how a company’s shares ultimately become available on the open market.

The months before an IPO are filled with preparation for pricing the offering. In addition to refining the company story prior to a roadshow, companies will often work with underwriters to determine the appropriate price range to include in the registration statement and the size of the offering.

The registration statement is initially prepared and reviewed by the SEC in draft form with pricing information excluded from the document. As the roadshow approaches, companies will amend the registration statement to include pricing information. During this time, underwriters will work with company management to understand the company’s capitalization table1 to determine an appropriate price range for the shares offered.

Oftentimes the underwriters will recommend that the company execute a stock-split or reverse stock split to bring their shares within a price range that is deemed favorable to investors. For example, underwriters often attempt to avoid pricing an IPO with a single-digit share price to avoid the risk of being delisted on some exchanges. Companies should be aware that employees with share-based compensation can react negatively when they suddenly hold fewer shares despite still owning the same percentage of the company. Additionally, the execution of stock splits often places a heavy burden on finance and legal teams.

Once an offering range is determined, the registration statement will be updated with the preliminary price range, assuming the midpoint of the offering range. Once the registration statement is amended and filed, the company can begin the roadshow.

It is not uncommon for pricing to change throughout the roadshow prior to final pricing. Finance teams should develop a spreadsheet that can quickly recalculate and reflect updated pricing information throughout the registration statement. Additionally, upon completion of the offering, a final prospectus will need to be filed with the SEC to reflect final pricing.

One of the most important events in the weeks leading up to the IPO is the road show. During a road show, company management pitches the company to institutional investors to generate interest in the offering. As mentioned previously, the company will have set a price range in an emended prospectus which will serve as the starting point in pitches to investors. During and after the roadshow the underwriters gauge demand for a company’s stock by receiving bids from institutional investors. This process, known as book building, helps underwriters know how to set the final offering price—the price at which the shares will be sold to institutional investors. The bids will almost always exceed the number of shares available; which is known as oversubscription. In fact, if the book is not oversubscribed the company will likely have to drop the offering price to sell all the shares planned in the offering.

The day before the IPO, the underwriters and board of directors of the company set the final offering price. The underwriters and company agree on a final price by analyzing the offers received from institutional investors. The strength of demand for the shares as well as the mix of investors at each price are the strongest factors in determining the final offering price. Once the price is set, the underwriters receive the shares from the company and will generally earn a commission of 5 to 7 percent of the total offering amount. At this point, the company knows exactly how much money it will raise in the offering, regardless of price fluctuations that will occur once trading begins.

Although the company knows how much money it will raise, price changes on the day of the IPO will have a large effect on current shareholders and new investors. On the morning of the IPO, shares are allocated to investors and price discovery begins once the market opens. Later, trading begins on the open market and underwriters may engage in price stabilization activities.

With the offering price set and the investor bids received, the underwriters will spend the morning determining how to allocate shares to investors. As mentioned previously, the bids from institutional investors should exceed the number of shares available. Therefore, the underwriters cannot simply give everyone the number of shares they bid for; instead, they will allocate shares based on the expected behavior of potential shareholders. Underwriters will avoid allocating too many shares to investors who are expected to unload the company’s stock because this could drive the stock price down. On the other hand, underwriters will not sell exclusively to long-term holding investors because if shares are not sold, a liquid market will fail to develop. Ultimately, underwriters try to allocate shares to a good mix of investors to ensure healthy prices and liquid markets for the stock. Each underwriter will get a certain number of shares assigned to them based on the underwriter agreement and their level of involvement in the IPO process. This allocation determines the amount of commission that each underwriter receives.

Company executives may be invited to ring the stock exchange bell on the morning of their IPO to signal the beginning of the trading day. However, trading on the IPO will not immediately begin. As trading commences on other stocks, the stock exchange begins to receive and record offers to purchase and sell the company’s shares from the open market. The company will also select a designated market maker who assists in this process by ensuring that a market for the stock develops by providing price quotes to traders. The major exchanges use a combined effort of machines and human judgment to determine an equilibrium price, which will become the opening price2 for the stock. This process takes the NYSE only 11 minutes on average, but will often take longer, especially for high-profile IPOs.

Once the opening price is set, the exchange matches up buyers and sellers, and the company’s stock finally begins to trade hands on the open market. Bids and offers will continue to come in throughout the day, and although the stock exchange takes special care to determine an equilibrium opening price, first-day trading on IPOs can be very volatile.

Although trading on the company’s stock is underway, many shareholders cannot immediately begin trading stock because of lock-up agreements. Lock-up agreements prohibit founders, employees, and some other early investors from selling their shares for a certain time after an IPO, usually 180 days. Lock-up agreements are important because (1) they help stabilize the stock price and (2) they help ensure that the incentives of management remain aligned with the performance of the company.

To stabilize volatility in the first day of trading, most underwriting agreements contain greenshoe provisions. A greenshoe option allows underwriters to purchase and sell additional shares—usually up to 15 percent of the original offering. Underwriters will exercise the greenshoe option if demand for the company’s stock exceeds supply. By increasing the supply of shares, the underwriter can smooth out price fluctuations. Alternatively, if demand for the company’s stock is weak and the price drops, the underwriter can repurchase shares from investors to boost the stock price.

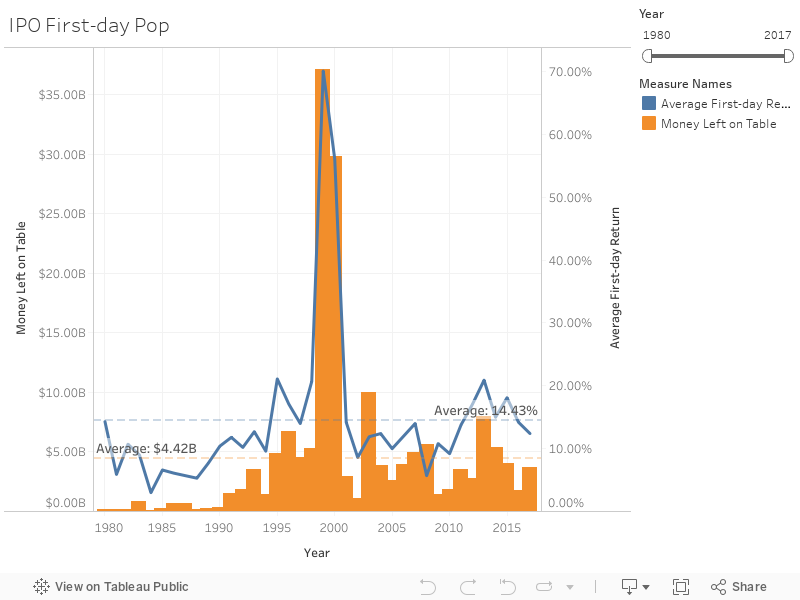

Often, the IPO company’s stock will see a high return on the first day of trading. This return is referred to as the first-day “pop” because of the expected increase in share price. Historically, the first-day pop on IPOs is around 14 percent. The following chart shows the average first-day return and aggregate money left on the table for IPOs since 19803.

As this graph shows, average first-day returns have been positive during every year since 1980, even reaching as high as 70 percent at the height of the dot-com bubble.

High first-day returns have certain advantages and are often viewed as a measure of an IPO’s success. A rapid increase in share price rewards institutional investors, which strengthens company-investor relationships and compensates institutional investors for their efforts to appropriately value the company. A strong relationship with investors can be especially important if the company is planning a secondary offering in the time following the IPO. Additionally, a large first-day return increases company morale as company employees and founders see their holdings appreciate. Finally, the first-day pop is often good publicity for a new public company.

Despite these advantages, there are some drawbacks if the first-day return is excessive. One of the major disadvantages of an excessive first-day pop is that the company going public does not receive the maximum amount of capital that the IPO could have raised—institutional investors and other shareholders benefit from the increased value of the shares. In other words, the company has left money on the table that they could have received had they priced their shares higher, at the prevailing market price. In addition to leaving money on the table, large first-day returns can also create unrealistic expectations and lead to a price correction in the months following the IPO.

Usually about three days after the IPO has been executed, the transaction is closed after final due diligence procedures have been completed. During this process, the company receives the proceeds of the offering from the underwriters after the underwriters have taken their commission.

Proper pricing is critical to a successful IPO—price too high and you may be unable to sell your stock, but price too low and you will leave a significant amount of money on the table. Understanding the events leading up to and occurring on the day of your IPO can help you know what to expect in these high-stress situations. Effectively marketing your stock to investors, selecting the proper mix of institutional investors, and understanding the implications of first-day pop will help you receive a favorable price for your company’s shares.